[ad_1]

Whereas North America and Europe debate the inevitable cashless future, the Asia-Pacific (APAC) area has already skilled a outstanding shift within the adoption and utilization of other cost strategies (APMs) in recent times.

The surge in digital wallets, eCommerce, and rising applied sciences has propelled the area to the forefront of the worldwide cashless revolution.

This text supplies an summary of the present APAC funds panorama, highlights well-liked cost strategies throughout varied nations, and discusses the impression of APMs on the general procuring expertise.

APAC Funds Overview: Low Penetration of Conventional Banking

In China, customers pay with both WeChat or Alipay – two of the nation’s favorite cost platforms that deal with 94% of China’s US$5 trillion cell pockets transactions yearly. Inside India, cell transactions have doubled after the federal government made 500 and 1000 rupees unlawful tender.

In Korea, the rise of TPay, a system that clears US$435 a month for approved funds utilizing cell service information, has helped the nation change into virtually utterly cashless.

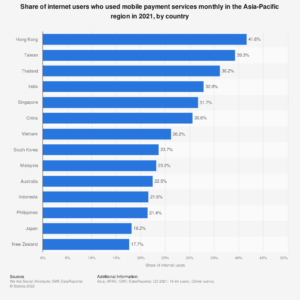

With none doubt, the APAC area is main the adoption of those new various cost methods by means of the usage of rising applied sciences and fuelled by altering client procuring behaviors – with 95% of Asia-Pacific customers procuring on-line repeatedly.

This development additionally exhibits its presence within the West, with Caesars Leisure, a Las Vegas lodge and on line casino expertise, integrating WeChat as a cost program, permitting visiting Chinese language vacationers to make use of their WeChat Pay inside their amenities.

One other issue fueling the accelerated shift wards digital funds was the COVID-19 pandemic, as customers and companies alike have sought contactless and environment friendly cost options. In China alone, the eCommerce market elevated by 17% and continued to develop throughout the pandemic, with Gen-Z consumers making up 56% of latest web procuring customers.

The drive to undertake AMPS within the APAC area has led to the next rising key cost tendencies: providing unmatched cost processing, utilizing non-public information to personalize buyer experiences, constructing long-term cost methods, and quickly shifting away from money.

However whereas these developments could — and to some extent will — affect how we pay globally, variations in cost providers are inevitable and obligatory. Finally, funds are like languages. And what’s working in China, South Korea, and different Asian-Pacific nations received’t essentially work elsewhere.

Well-liked Fee Strategies in APAC

The various and huge client base in APAC nations has led to the emergence of assorted well-liked cost strategies catering to the distinctive wants of every market:

China – AliPay and WeChat

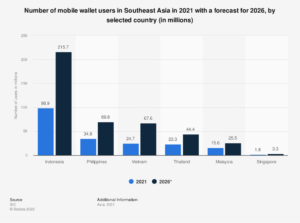

In China, AliPay, operated by Ant Group, is the most utilized digital cost app. In the meantime, Southeast Asia is witnessing a surge in digital cost adoption, with rising startups like Indonesia’s Gojek and Singapore’s Sea platform gaining traction.

A Rakuten Perception survey in October 2022 revealed that GoPay by Gojek was the most popular e-payment service in Indonesia, utilized by 78% of respondents. Moreover, PayPal dominated the Southeast Asian market, with a big presence in Indonesia, Malaysia, the Philippines, Singapore, and Vietnam.

Rise up-to-date market metrics and insights that can assist you enter the Chinese language eCommerce market and tackle established regional gamers.

Globally, nations are following go well with and embracing their very own variations of digital cost strategies:

India – UPI (Unified Fee Interface)

UPI is amongst India’s main various cost platforms, accounting for 10% of the nation’s retail transactions. This real-time cost system allows customers to conduct P2P or P2M transactions through their cell units.

Moreover, UPI is built-in with different nations’ methods, corresponding to Singapore’s PayNow, Bhutan’s BHIM app, and Nepal’s NIPL.

Get the insights and steering wanted for getting into and attaining traction within the Indian eCommerce market.

Australia – POLi

Australia’s developed economic system, minimal restrictions on imports, and plentiful pure sources set the stage for cashless transactions to change into the norm by 2025.

POLi is another cost methodology that permits companies to obtain funds instantly into their financial institution accounts.

Learn how to enter the Australian eCommerce market right here.

Thailand – TrueMoney

In Thailand, TrueMoney is the go-to e-wallet, boasting over 15 million customers and enticing low acceptance charges. A Visa research revealed that 9 out of 10 Thai customers choose cashless funds, pushed by COVID-19 issues and the rising variety of companies providing cashless choices.

TrueMoney supplies a safe and handy cashless expertise and empowers customers to pay payments, switch cash, e-book points of interest, and extra.

Bangladesh – bKash

Though Bangladesh was gradual to undertake digital funds, the COVID outbreak accelerated this shift. Regardless of challenges like monetary exclusion and belief points, the nation’s central financial institution anticipates continued development in digital funds, together with bKash.

As a cell monetary service, bKash permits customers to deposit cash into their cell accounts and entry varied providers corresponding to invoice funds and cash transfers.

Pakistan – Easypaisa

EasyPaisa, launched in 2009, is a mobile-based cost service in Pakistan that caters to Telenor Pakistan cell phone customers. Rating because the world’s third-largest cell cash deployment – enabling customers to pay payments, switch funds, and entry authorities advantages. This versatile service streamlines transactions for customers throughout Pakistan, aligning with the rising development of other cost strategies.

Shifting ahead, understanding how APAC nations deal with APM adoption shall be essential for companies seeking to supply seamless cost experiences on this numerous area.

How APAC nations face the APM adoption

The usage of APMs is strongest within the APAC areas – reflecting the area’s numerous inhabitants’s distinctive preferences and wishes. Customers overwhelmingly choose eWallets, financial institution transfers, and cash-on-delivery choices over conventional cost strategies.

Let’s take a look at a few of the causes behind this.

Modernizing Legacy Infrastructure and ISO 20022

Nice system adjustments have their fair proportion of issues. With the more and more widespread adoption of smartphones and customers’ preferences to make use of eWallets, conventional legacy banking methods are lagging – they merely had been by no means designed to deal with the pressures of 24/7/365 real-time transactions.

The necessity to replace the system is clear. Banks within the APAC area are scrambling to maneuver in direction of the brand new ISO 20022 commonplace, which can contain processing bigger information volumes quicker for real-time funds, every day liquidity administration, fraud detection, and compliance checks.

Nonetheless, consumer adoption remains to be a problem, with a research displaying that implementation of user-focused expertise will finally result in wider acceptance of a very cashless society.

Smartphones and eWallets are influencing APAC’s cost processing panorama

China accounts for the highest utilization of smartphones on the earth, with over 865 million customers. India is trailing not too far behind, with 606 million customers. Moreover, the nation’s rising adoption charge of the Web and digitizing market sector in India are influencing residents’ APM utilization.

Each of those nations have adopted eWallets providing cost comfort and safety. Consequently, many banks and cost processors are actually re-evaluating their enterprise methods, particularly in enhancing their present infrastructure, as talked about earlier than, to maintain up with their client base and retain market share.

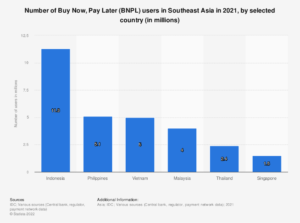

Purchase Now, Pay Later (BNPL) in APAC

The emergence of BNPL options has additional reworked the funds panorama within the area. In response to Statista information, these versatile financing choices have gained traction in APAC, offering customers with handy and accessible options to conventional credit score merchandise.

The “Purchase now, pay later” development has skilled a big increase among the many Gen Z and Millennial workforce; nevertheless, this development could wane as financial circumstances decelerate.

Moreover, it’s anticipated that APAC nations will comply with within the UK authorities’s footsteps in implementing stricter rules on BNPL, which may additional impression its future prospects.

Various Fee Strategies in APAC

This altering panorama calls for an in-depth understanding of client preferences and the market’s route for companies searching for a frictionless cost expertise within the Asia-Pacific area.

There’s a notable urge for food for innovation in APAC, with growing markets corresponding to Malaysia, India, Thailand, and Indonesia demonstrating a increased adoption charge of APMs. These customers, who contemplate themselves tech-savvy, are eager to search out the proper options for his or her wants.

Though playing cards and card-powered wallets stay well-liked in developed APAC nations like Japan, Taiwan, Singapore, and South Korea, the choice for eWallets and financial institution transfers has elevated considerably throughout the area.

Some rising economies are bypassing the cardboard stage altogether and searching for out new methods to pay on-line.

The multitude of APMs used throughout APAC, corresponding to Paytm in India, OVO Pockets in Indonesia, True Cash in Thailand, and Maybank2u in Malaysia, presents each alternatives and challenges for companies.

As their recognition surges globally, companies should preserve their finger on the heart beat, adapting to ever-changing markets and client preferences.

APMs and the Seamless Buying Expertise

APMs are extra than simply numerous cost choices; they’re designed to combine seamlessly into the shopper expertise, catering to numerous preferences. This tailor-made strategy enhances buyer satisfaction and encourages repeat transactions whereas decreasing friction within the checkout course of and leading to increased conversion charges for on-line retailers.

Furthermore, APMs have the potential to revolutionize the procuring expertise. For instance, Singapore’s PayNow, a peer-to-peer funds switch service initially accessible to retail prospects, has expanded its scope to incorporate companies and retailers.

By enabling on the spot funds by means of a easy QR code scan or cell quantity enter, PayNow eliminates the necessity for getting into prolonged checking account particulars, making transactions quicker and extra handy. This ease of use promotes a smoother procuring expertise and fosters cashless transactions nationwide.

By incorporating APMs like PayNow into their cost choices, companies can create a seamless procuring expertise that meets the wants and preferences of their prospects, finally boosting satisfaction and driving repeat enterprise.

Conclusion

The rise of other cost strategies within the APAC area has revolutionized the eCommerce panorama, offering customers with many choices that cater to their distinctive preferences and necessities.

Because the area continues to steer the international cashless revolution, companies should adapt and embrace these rising applied sciences to stay aggressive and meet the evolving wants of their prospects.

Within the face of an more and more digital world, APAC’s speedy adoption of APMs serves as a testomony to the transformative energy of expertise and its potential for reshaping international commerce. And as this area continues to innovate and push boundaries, the remainder of the world will comply with go well with, resulting in a extra linked, handy, and safe future for all.

[ad_2]